For 25 years in the ballroom of the Hilton Hotel in midtown Manhattan, a sprawling, week-long conference you’ve never heard of shaped your financial life. It was called the Securities Industry Association Technology Conference, (later renamed SIFMA Tech) and it was where the largest technology firms came to pitch the biggest banks on everything from how your 401k got traded to how your bank let you access your money online. Of course, ‘you’ were merely a notional statistic at this four-day financial love-fest. The real name of the game was to help the banks get more profitable and give institutional traders an edge over their – equally institutional – competition.

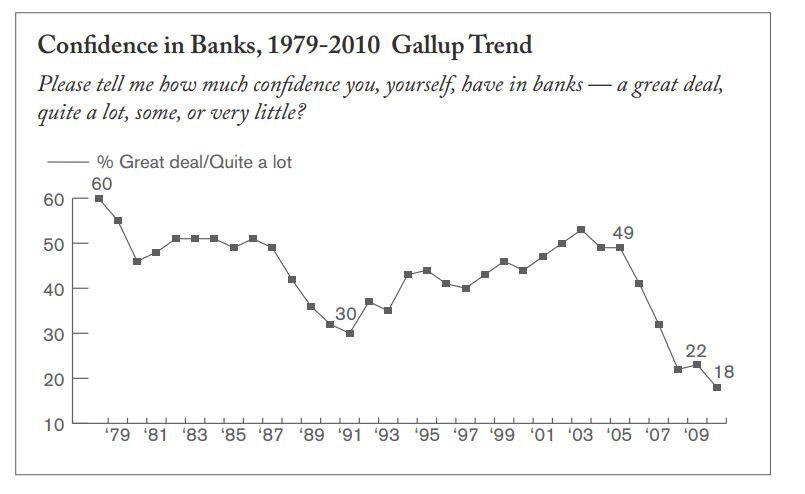

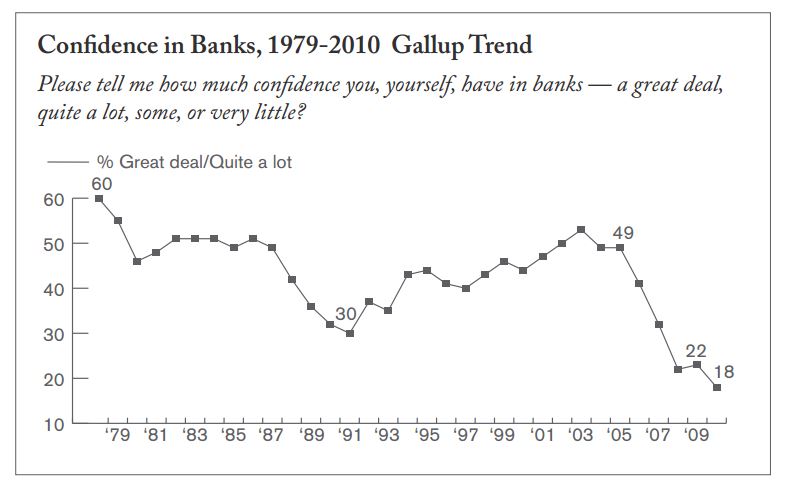

But then 2008 happened and the financial world went to hell in a hand basket, taking the majority of SIFMA Tech with it. Not only did the banks suffer but public trust in banks plummeted to somewhere just slightly north of used car dealers.

Financial services didn’t just take a beating during the financial crisis, the fundamental nature of finance needed a makeover. Enter Finovate. Finovate is like TechCrunch Disrupt for Finance, showcasing the best new innovations in financial and banking technology via short, fast-paced demos (no slides allowed) and high-quality networking.

Its location? The ballroom of the Hilton Hotel in midtown Manhattan.

The Finovate conference, like the SIFMA show before it, still brings together financial bigwigs and technologists but ‘you’ – meaning the consumer: your hopes, dreams and desires – are now most definitely the center of the action. Walking through the halls of Finovate has a somewhat Twilight Zone quality about it. It’s like a version of Dickens’ ‘A Christmas Carol’ in which the financial industry wakes up after a terrible nightmare and resolves to change its miserly ways before it’s too late.

As Stephane Dubois, CEO of financial data company and regular exhibitor, Xignite points out: “There is an incredible irony to seeing Finovate held at the Hilton, the traditional home of the SIFMA Tech show. The energy and innovation demonstrated by these new companies at Finovate easily offsets the luster lost over the years by SIFMA and its traditional contingent of legacy financial providers. It’s like watching a phoenix being born out the ashes of old finance.”

So just who are these financial philanthropists?

Well there’s SaveUp, an app on a mission to help consumers rebuild their finances after five years of recession. Describing themselves as ‘the gummy vitamin of personal finance’, SaveUp blends traditional balance updates with gamification, encouraging consumers to pay down debt with the opportunity to win prizes and merchant-funded rewards.

In the same vein, an app called ImpulseSave from True Potential enables users to make “impulse deposits,” in small increments on their cellphones, smart watch and evenGoogle GOOGL +0.61% Glass. The ideas is to make saving habitual and even fun.

“Traditional banks could never have approached saving this way” says Jeff Burrow, COO and Co-founder of FlexScore, another Finovate exhibitor and presenter. “The reality is that old-school financial institutions make their money on debt. They are not really incentivized to help consumers become debt free.”

Then there’s EverSafe, a financial monitoring platform designed specifically to protect seniors from fraud. “Isn’t this what the banks and credit bureaus are supposed to be doing?’ I ask. “You would think so” says Howard L. Tischler, EverSafe’s founder and CEO, with a wry smile “but we’re definitely filling a gap in the market!”

SIFMA Tech didn’t exactly get replaced with a bunch of financial Mother Theresas but this brand of financial capitalism certainly comes in a different flavor. Even the less overtly benevolent exhibitors promote a democratization of finance that was scarce before 2008; giving consumers access to instruments and models previously the preserve of the institutional market alone.

HedgeCoVest, one of the most popular exhibitors at the show, is a platform which enables investors to make allocations to hedge fund strategies in their own brokerage accounts, thus giving mom and pop a taste of alternative assets and the higher returns they typically deliver.

Evan Rapaport, CEO of HedgeCoVest notes: “The individual investor has been locked out of this part of the market for too long. We believe that the most attractive investment opportunities should be available to everyone and not just institutions and the ultra-wealthy”

Patch of Land, does the same thing in property, using a peer-to-peer model and enabling the mass affluent in becoming savvy real estate investors with investments as low as $5000.

“The established principles of finance were overdue for a rethink” says Jeff Burrow of Flexscore. “For example, we created Flexscore because we believed that credit worthiness – the traditional gauge of a person’s financial wellbeing – was a useful but ultimately limited measure of overall fiscal responsibility. Students come out of college and the first thing they’re told to do is get a credit or store card and start establishing a credit history. If you think about it, that’s crazy: we’re telling kids who are probably already overloaded with college debt to go and start borrowing more money.” Flexscore, Financial Life Experience Score, by comparison, takes a more holistic view of the individual, gives them total financial clarity and helps them improve their financial standing.

This concept of clarity and accessibility permeates the halls of Finovate. Firms such asblooom (sic), for example, are attempting to make the complex world of 401ks more comprehensible for non-financial customers via neat, consumer-friendly visualizations.

Even in the most arcane areas of the institutional market, such as fixed income, new players like Algomi (which I heard referred to at the show as “Facebook for Bonds“) are borrowing tools pioneered in social media to bring an openness to the financial markets.

At the end of the first day I spoke to Mike Laven, CEO of Currency Cloud, another new financial provider and regular Finovate attendee. Unlike many of the presenters at the show, however, Mike is an industry veteran – having held multiple C-suite positions at financial technology firms since the early 90s. I asked him why, after all that time at the top of large, well-established providers he chose to launch a scrappy start-up. ‘Taking another CEO role at a major firm would certainly have been the easier choice” he concedes, “but there’s a financial technology revolution happening today and I want to be on the right side of history.”