As we approach 2015, bank accounts, like cellphones or those annoying Facebook quizzes, seem like something we should take for granted as part of the fabric of our life. Yet you may be surprised to learn that more Americans actually own and operate a cellphone (90%) than have a bank account (80%). In fact, there’s a lot about banking today that might surprise you.

According to the FDIC and my friends at PayNearMe here are some pretty shocking statistics:

- 50 million US adults don’t have a bank account at all (That’s more than don’t have health insurance — 41 million)

- 68 million are ‘underbanked’ i.e. they may have a bank account but rarely use it, instead relying on cash transactions or alternative financial service providers

- A quarter of US households are financially under-served

“Aha!” I hear you cry “but unbanked is like undocumented right? These are probably illegal immigrants we’re talking about!” Well, actually, no. 80% of the unbanked are USborn citizens. 43% of them own their own homes. 50% of them are white (compared to 26% Black and 20% Hispanic). And 27% of them make over $50,000 per year.

Still not surprised? How about the fact that unbanked or underbanked are 30% more likely to use mobile payments than the rest of society. Or that 57% of them own a smartphone compared to only 44% of the overall US population. Starting to sound less and less like the stereotypical undocumented migrant worker to me.

The underbanked market is a vast (with a buying power of more than $1 trillion annually) but rarely discussed. At over a third the size of the Federal budget, it is a shadow economy which encompasses a growing number of young, digitally savvy, millennials with entrenched dislike and distrust of the traditional financial services model.

Luckily for them there’s Money 20/20. The Money 20/20 conference is to financial services what TechCrunch Disrupt is to technology design and development. Over 10,000 people gathered in Vegas 3 weeks ago to discuss the latest in payments, ecommerce and financial innovation – and what I noticed there, besides the amount of money I lost at the blackjack tables, was the sheer number of providers who are trying to create a better world for the underbanked.

PayNearMe for example enables users to pay bills in cash at local stores, like 7-Eleven or Family Dollar without having to use the gas money to drive to the bank.

Paytoo, another exhibitor at the show, has created a mobile wallet solution for the unbanked which along with classic banking services like bill pay and direct deposit is offering unbanked consumers access to leasing and vacation financing packages.

GlobeOne also offers banking to the unbanked via a mobile app but has additional cool features like free international wire transfers, no late fees or minimum balance and below market interest rates. In addition, 50% of the interest GlobeOne earns is reinvested into its community of users.

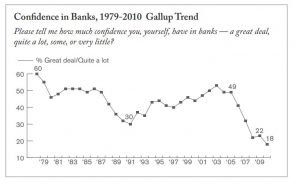

But why are so many people seeking out alternatives to a system that has stood for the best part of 4000 years? Well, the consensus seems to be because people think banks are mostly terrible.

Results of a survey released last week show that, currently, only 13% of Americans believe bank systems are capable of preventing another scandal. And according to this New York Times article traditional banks are actually becoming more expensive to use. Only 39% of noninterest-bearing checking accounts were free in 2011, down from 76% in 2009. You read that right; during the worst period in banking since the Great Depression, over a third of banks have removed free checking options on non-interest bearing accounts.

Oh, and the average overdraft fee is now $32.74.

The article tells one particularly illuminating story of a professor who took his daughter to open a savings account at their local bank:

“We put in $50, and I had the idea that we would go to the bank every month and make a deposit. We would watch the money grow along with interest. The next month we went back to make the next deposit, and lo and behold there was only $45 in the account. Turned out that the bank was charging for low balances. End of lesson.” He got the bank to return the $5 and closed her account — and his own.

Against this backdrop it isn’t surprising that the young and relatively affluent are joining the ranks of those looking for a better way to manage their money.

I’ve talked before about the gap that traditional banks are creating through a lack of innovation. As long as they continue to stagnate, millions of Americans will continue to seek out alternative solutions and conferences like Money20/20 will continue laughing all the way to the un-bank.